Only 15% of San Diego households can qualify for the median-priced home. That single number scares most people away from the conversation entirely. It should not. If you know where to look and which programs to use, a single buyer earning $118,000 a year can qualify for a condo in City Heights, and a dual-income household at $160,000 combined can buy a single-family home there too.

This is the affordability breakdown I walk every client through before they start touring homes. Real qualifying income at every San Diego price tier, actual monthly payment numbers (not just the P&I that online calculators show you), down payment and closing cost math, and the three programs that meaningfully change these numbers for first-time buyers, veterans, and moderate-income households.

How Lenders Calculate What You Can Afford

Photo: Towfiqu barbhuiya / Unsplash

Lenders do not approve a loan based on your salary alone. They care about one number above all else: your debt-to-income ratio (DTI). The standard most lenders use is the 28/36 rule.

- 28% front-end ratio: Your total monthly housing cost (principal, interest, property taxes, homeowners insurance, and HOA fees if applicable) should not exceed 28% of your gross monthly income.

- 36% back-end ratio: Your total monthly debt, including housing plus car payments, student loans, credit cards, and any other recurring obligations, should not exceed 36% of your gross income.

In practice, many conventional lenders will approve at a 43 to 45% total DTI for strong borrowers, and FHA allows up to 57% in some cases. But the 28% front-end is the anchor for qualifying income calculations, and it is what I use throughout this guide.

The other critical inputs are your down payment and your interest rate. A larger down payment reduces your loan balance and eliminates PMI once you clear 20%, both of which lower the income you need to qualify. The current average 30-year fixed rate in San Diego is 6.55%. VA loans are averaging 5.95%, and well-qualified borrowers using certain lenders are seeing conforming rates as low as 5.5%.

Property taxes in San Diego County run approximately 1.1% of the purchase price annually. On a $1,100,000 home, that is $1,008 per month before insurance. Most buyers relocating from outside California are not prepared for that number. If you are moving to San Diego from out of state, this is one of the first things to build into your budget.

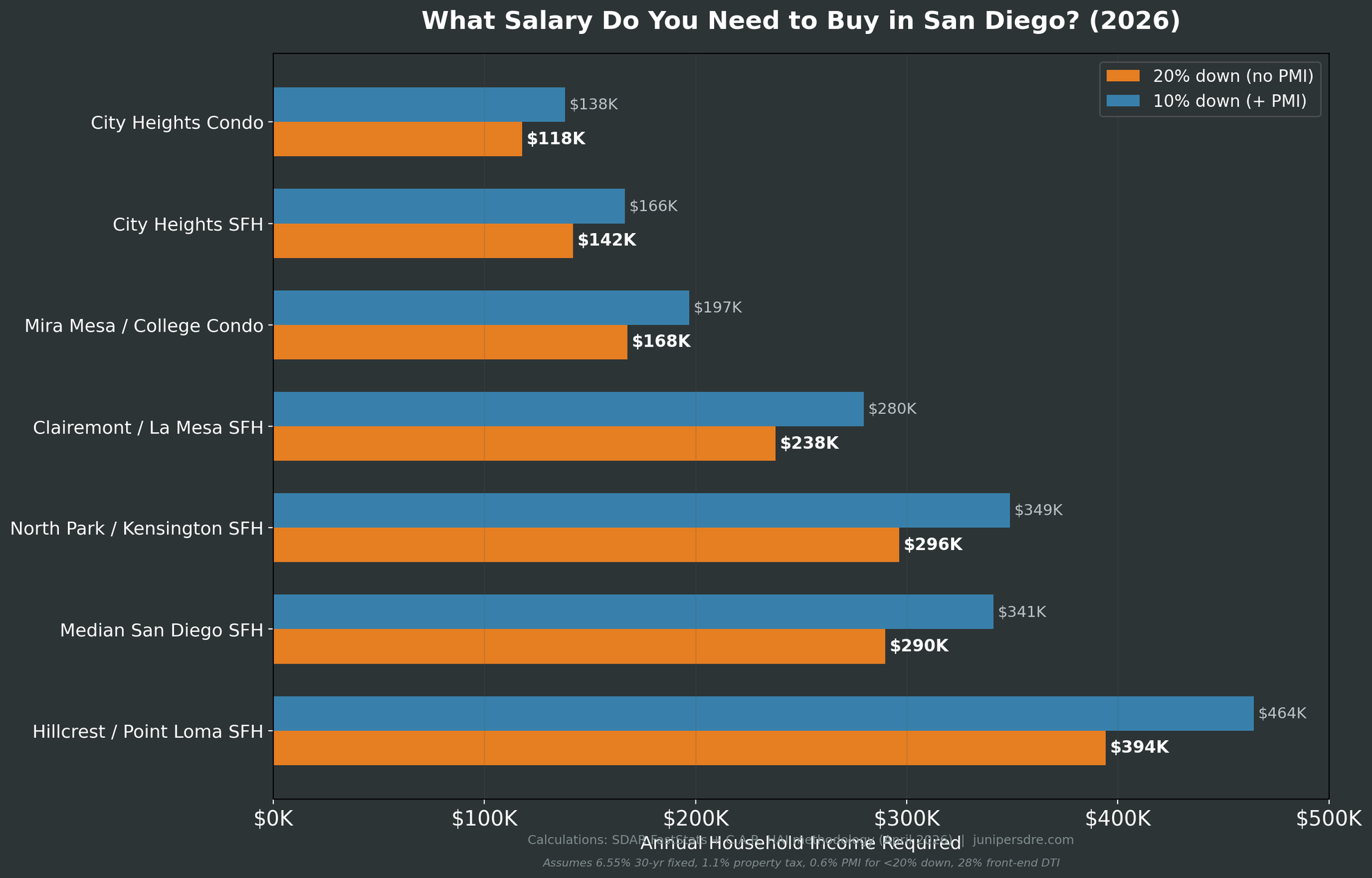

What Salary You Need at Every Price Tier

The table below translates San Diego price points into required qualifying income. All calculations use the 28% front-end rule, a 6.55% 30-year fixed rate, 1.1% annual property tax, and standard insurance. The 20% down scenario eliminates PMI; the 10% down scenario adds 0.6% annual PMI on the loan balance.

| Neighborhood / Property Type | Price | 20% Down, Income Needed | 10% Down, Income Needed | Down Payment (20%) |

|---|---|---|---|---|

| City Heights / College Area, Condo | $438K | ~$118K | ~$138K | $87,600 |

| City Heights, SFH | $530K | ~$141K | ~$165K | $106,000 |

| Mira Mesa / Clairemont, Condo | $630K | ~$167K | ~$197K | $126,000 |

| La Mesa / Clairemont, SFH | $900K | ~$238K | ~$280K | $180,000 |

| Median San Diego SFH | $1.1M | ~$243 to 290K | ~$341K | $220,000 |

| Hillcrest / Point Loma, SFH | $1.5M | ~$394K | ~$464K | $300,000 |

Rate: 6.55% 30-yr fixed. Property tax: 1.1%/yr. PMI: 0.6%/yr for 10% down. 28% front-end DTI. | Swipe to see all columns →

Two things stand out. First, the entry-level condo in City Heights or College Area requires roughly $118,000 a year, well within reach for a single tech, healthcare, or government worker in San Diego. Second, the jump between 20% and 10% down is significant. On a $1.1M home, going from 10% to 20% down saves you nearly $100,000 per year in qualifying income requirement because PMI on a $990,000 loan adds $495 per month and the larger loan adds $600+ per month in P&I.

For a neighborhood-by-neighborhood breakdown of current home prices, see the best neighborhoods in San Diego guide.

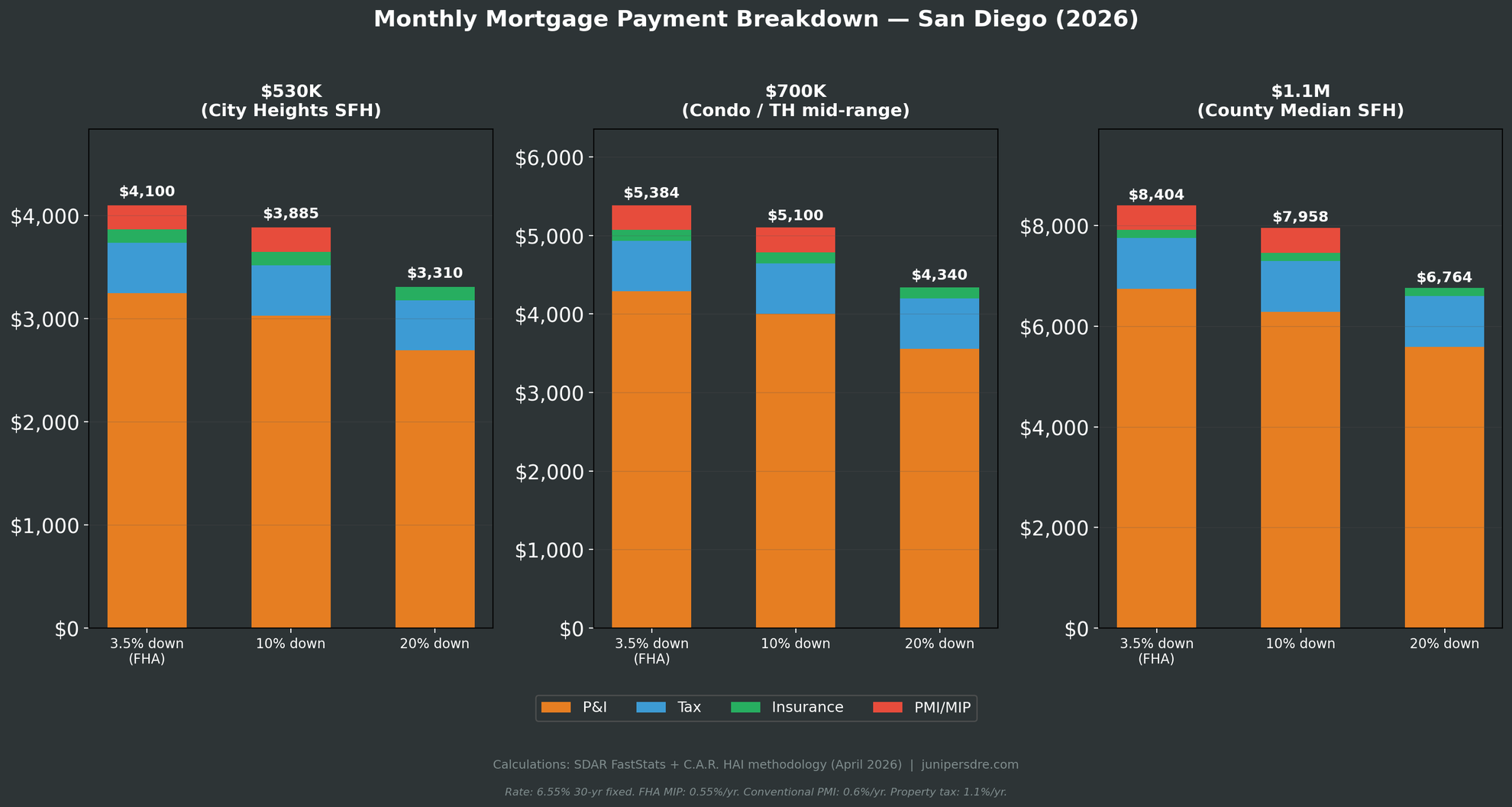

Monthly Payment Breakdown by Price and Down Payment

Most online calculators show you a principal and interest number and stop there. The real monthly cost in San Diego is always higher once you add property taxes, insurance, and PMI. Here is the true all-in monthly cost at three representative price points.

The chart above shows total monthly housing cost broken into four components: principal and interest, property taxes, homeowners insurance, and PMI or FHA mortgage insurance. A few things worth calling out:

- At $530,000 with 3.5% FHA down, your total monthly payment runs approximately $3,700. That is $100 to $300 more per month than renting a comparable apartment in the same neighborhood, but you are building equity instead of paying a landlord.

- At $1.1M with 10% down, the monthly payment exceeds $7,900 before HOA. That is the number a lot of buyers underestimate by $1,000 to $1,500 per month compared to what an online P&I calculator shows them.

- The PMI cost for 10% vs 20% down on a $1.1M home is approximately $495 per month. Over five years before refinance, that is $29,700 extra. But preserving $110,000 in cash at closing has its own strategic value, especially in a competitive market where inventory is dropping.

How Much Cash Do You Actually Need at Closing?

Photo: Pexels

Down payment is only part of the cash you need. Closing costs in California typically run 2% to 3% of the purchase price and include lender fees, title insurance, escrow, and prepaid property taxes and insurance. Here is the full cash picture at each price tier.

| Price | Down (3.5%) | Down (10%) | Down (20%) | Closing Costs (~2.5%) | Total Cash, 20% Down |

|---|---|---|---|---|---|

| $438K | $15,330 | $43,800 | $87,600 | $10,950 | $98,550 |

| $630K | $22,050 | $63,000 | $126,000 | $15,750 | $141,750 |

| $844K (C.A.R. entry-level) | $29,540 | $84,400 | $168,800 | $21,100 | $189,900 |

| $1.1M (county median) | N/A (above FHA limit) | $110,000 | $220,000 | $27,500 | $247,500 |

Closing costs estimated at 2.5% and vary by transaction. FHA loan limit for San Diego County 2026: $1,104,000. | Swipe →

The savings gap is real. A buyer targeting a $630,000 condo with 20% down needs $141,750 liquid before making an offer. A buyer using 10% down needs $78,750 ($63K + $15.75K closing costs), but then carries PMI at roughly $315 per month until the loan balance drops below 80% of the value. At current prices, that takes approximately 8 to 10 years without additional paydown.

Programs That Change the Math: CalHFA, VA, and SDHC

Three programs can meaningfully shift the affordability calculation for San Diego buyers. Not everyone qualifies, but for those who do, these are significant advantages.

CalHFA MyHome Assistance Program

California Housing Finance Agency’s MyHome program provides a deferred-payment junior loan of up to 3.5% of the purchase price (for FHA first mortgages) or 3% (for conventional) to cover down payment and closing costs. It is a deferred loan with no monthly payment, repaid when you sell or refinance. To qualify: first-time buyer (no home ownership in the past three years), primary residence, complete homebuyer education, and meet income limits. For San Diego County, the 2025 CalHFA income limit for first mortgages and subordinate loans is $258,000. There are no sales price limits. Minimum credit score: 640 for FHA, 680 for conventional.

Practical impact: on a $530,000 purchase with FHA, CalHFA MyHome can cover the full $18,550 FHA down payment requirement (3.5%), leaving you with only closing costs as your out-of-pocket expense. Pair it with a seller credit for closing costs and some buyers are getting into homes for under $10,000 cash.

VA Loans: The Most Powerful Tool for Veterans

San Diego has one of the largest active-duty and veteran populations in the country. VA loans offer zero down payment, no private mortgage insurance, and competitive rates, currently averaging 5.95% in San Diego versus 6.55% for conventional. The VA conforming loan limit for San Diego County in 2026 is $1,104,000 for eligible veterans with full entitlement. Above $1,104,000 requires a down payment of 25% of the excess.

On a $1,100,000 home, a VA loan at 5.95% with 0% down produces a monthly P&I of approximately $6,551, versus $5,592 for conventional at 6.55% with 20% down. The conventional buyer put in $220,000 cash. The VA buyer put in $0 and pays $959 more per month. But that $220,000 can instead be invested, deployed as a reserve, or used to buy a second property. I covered the full breakdown on VA loans in San Diego in a separate guide.

SDHC and County CalHome

The San Diego Housing Commission offers closing cost and down payment assistance for buyers purchasing within city limits. Price caps apply: approximately $650,000 for single-family homes and $450,000 for condos within City of San Diego boundaries. Income limits target 50 to 120% of area median income. SDHC requires a 3% minimum down payment, which can be entirely a gift or approved grant.

San Diego County’s CalHome program goes further. It provides a grant of up to 20% down plus $10,000 toward closing costs. No borrower cash required if you qualify. CalHome covers unincorporated county areas with higher price caps. The combination of CalHome + FHA means some first-time buyers are purchasing with effectively zero out-of-pocket cash.

What Two Incomes Unlock

Photo: Pexels

San Diego is fundamentally a dual-income market at the median. The county’s $243,600 qualifying income threshold is achievable for many two-income households where it would be out of reach for a single earner. Here is what specific income combinations unlock.

| Household Income | Example Combination | What It Buys (20% Down) |

|---|---|---|

| $120K combined | $65K + $55K (healthcare + admin) | City Heights condo, College Area condo |

| $160K combined | $90K + $70K (tech + teacher) | City Heights SFH, Mira Mesa condo, FTB entry-level range |

| $200K combined | $120K + $80K (engineer + RN) | Clairemont / La Mesa SFH, North Park condo |

| $260K combined | $150K + $110K (two engineers) | Median San Diego SFH, North Park SFH |

| $400K combined | $220K + $180K (two doctors / senior tech) | Point Loma, Hillcrest SFH, higher La Jolla condos |

Swipe to see all columns →

One important qualifier: lenders count both incomes toward DTI, but they also count both debt loads. If both borrowers carry significant student loans, car payments, or credit card minimums, the combined debt drag can offset the income advantage. Two incomes with clean balance sheets unlock far more than two incomes with combined $4,000 in monthly debt obligations.

What to Do If You Are Not There Yet

If the income numbers above are out of range, you have more options than you might think.

Start with condos, not single-family homes. The $118,000 qualifying income for a City Heights or College Area condo is achievable for a single buyer in many San Diego industries. A condo is not the house you will live in forever. It is the equity you build on the way to it. Many of my clients have moved from a $440K condo entry point to a $1M+ home in 5 to 7 years by leveraging the equity they accumulated.

Run the rent-versus-buy breakeven. On a $530,000 City Heights SFH at 6.55% with 5% down, your all-in monthly payment is approximately $3,800. A comparable rental in the same neighborhood runs $2,400 to $2,800. The monthly difference is real, but over five years even modest 3% annual appreciation adds $85,000 in equity, more than the total premium you paid. The San Diego market has not had a down five-year period since the 1990s.

Target the down payment gap with DPA programs. CalHFA MyHome covers the full FHA down payment at $530,000 and below, and SDHC adds closing cost relief within city limits. If you are at $100K to $160K household income, you may qualify for enough assistance to close with under $20,000 out of pocket.

If you are a veteran, use your VA benefit. The zero-down, no-PMI structure is the most powerful homebuying tool available in San Diego. A veteran couple at $180,000 combined income qualifies for roughly $800,000 to $900,000 with no down payment and no PMI. That covers most of San Diego’s mid-range market.

For a complete walkthrough of the first-time buyer process in San Diego, from pre-approval to closing, including neighborhood-by-neighborhood condo and SFH entry points with current MLS data, I have a full guide that covers it step by step. If you want to get oriented on the city first, the 2026 relocation guide covers cost of living, the job market, schools, and neighborhood comparisons.

Every buyer’s situation is different. The numbers above give you the framework, but your income, your debts, your savings, and your timeline interact in ways a table cannot capture. If you want to run your specific scenario, I am happy to walk you through it and tell you exactly where you stand in today’s market.

Miguel Chairez, Juniper Real Estate Co.

619.253.3333 | miguel(at)junipersdre(dotted)com

Contact Miguel | Buyer Services | Property Management

Frequently Asked Questions

What salary do you need to buy a house in San Diego?

It depends on which house. At the county median ($1,100,000 SFH), C.A.R. calculates a required income of $243,600 per year using Q4 2025 data. At current rates (6.55%) and the March 2026 median, the number is closer to $290,000. At entry-level condos in City Heights or College Area ($438K to $530K), the qualifying income drops to $118,000 to $141,000 per year with 20% down. VA loans and CalHFA assistance can lower these thresholds further.

Can I afford a house in San Diego on $100,000 a year?

At $100,000 per year, your maximum monthly housing budget under the 28% rule is $2,333 per month. That qualifies you for a purchase price of roughly $325,000 to $375,000, below the floor for San Diego single-family homes but within range of some condo products if you use FHA financing (3.5% down, $15,330 on a $438K condo) combined with CalHFA MyHome down payment assistance. City Heights condos start in the $380,000 to $440,000 range and can be reached at $100K income with an FHA loan and DPA program.

How much is a down payment on a $1 million house in San Diego?

A conventional 20% down payment on $1,000,000 is $200,000. With 10% down you put in $100,000 but add approximately $500 per month in PMI. The conforming (non-jumbo) loan limit for San Diego County in 2026 is $1,104,000, so a $1M purchase stays in conforming territory. Total cash to close including closing costs (estimated at 2.5%) is approximately $225,000 for 20% down or $125,000 for 10% down.

What is the minimum income to qualify for an FHA loan in San Diego?

FHA does not set a minimum income floor. It sets a maximum DTI ceiling (typically 43 to 57% total DTI). The practical floor is whatever income produces a 28% front-end payment that covers your mortgage. At San Diego County’s FHA loan limit of $1,104,000 with 3.5% down ($38,640), the loan is $1,065,360. Monthly P&I at 6.15% FHA rate is approximately $6,484, plus $1,008 taxes and $175 insurance = $7,667. Qualifying income: approximately $328,500/yr. For more accessible FHA purchases, a $530,000 home with 3.5% down requires approximately $145,000 to $155,000 per year.

Is it better to put 20% down or use the cash for other things?

The math depends on what “other things” means. If the alternative is sitting in a savings account, the 20% down wins: you eliminate PMI ($300 to $500/month on a $700K to $1.1M home) and you reduce your loan balance from day one. If the alternative is investing in a diversified portfolio returning 7 to 10% annually, the comparison is tighter, especially for VA-eligible borrowers who can put 0% down with no PMI at all. The right answer is specific to your tax situation, liquidity needs, and risk tolerance. Talk to a fee-only financial advisor and your lender before deciding.

Data sources: California Association of REALTORS® Q4 2025 Housing Affordability Index (HAI), SDAR FastStats (March/April 2026), Redfin Affordability Data (January 2026), CalHFA 2025 Income Limits (effective June 2025), San Diego County FHA Loan Limits 2026 (HUD), FHFA 2026 Conforming Loan Limits. Mortgage calculations use 6.55% 30-year fixed (San Diego market average April 2026, per Amortio). All figures approximate and for educational purposes.